Related News: Post-Credits: How EV Adoption Advances When Incentives Fade

EV Demand Plummets In October As Credits Expire

The shift marks a recalibration rather than a retreat, as the market adjusts to post-incentive conditions.

November 19, 2025

EV sales fell sharply in October as the market adjusted to the loss of federal tax credits, impacting both new and used segments.

Photo: Cox Automotive

3 min to read

October marked a major reversal in the electric vehicle market as the federal EV tax credit expired, ending three months of accelerated sales. Shoppers rushed to secure incentives before the deadline, but once it passed, demand dropped and inventories rose across both new and used EV segments.

EV Sales Fall Sharply in October

New EV Sales

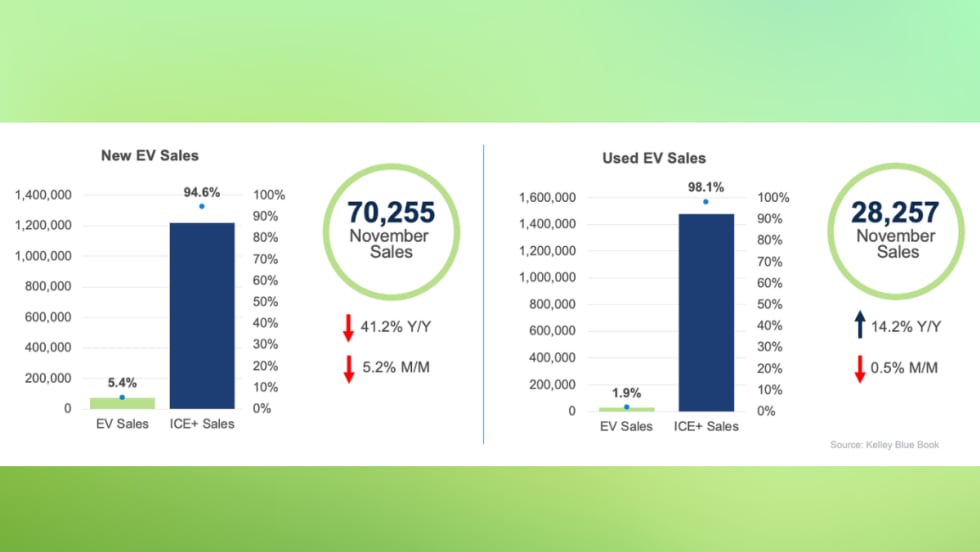

New EV sales totaled an estimated 74,835 units, down 48.9% from September’s record and 30.3% year over year. EV share of total U.S. sales fell to 5.8%, down from September’s 11.6%.

The decline spanned both luxury and non-luxury categories:

Luxury EV sales: down 39%

Non-luxury EV sales: down 65%

Top OEMs by volume:

Tesla: 40,650

Chevrolet: 5,910

Ford: 4,912

Cadillac: 4,344

Hyundai: 2,429

Despite a 35.3% month-over-month drop, Tesla’s share climbed to 54.3% as competitors saw even sharper declines. Rivian posted the mildest decline among major EV manufacturers at 14.7%.

Used EV Sales

Used EV sales reached 31,610 units, down 20.4% from September but up 36.2% year over year. Market share fell to 1.9%, a one-point decrease.

Top brands by used EV sales:

Tesla: 11,927

Ford: 2,273

Chevrolet: 1,919

Audi: 1,754

BMW: 1,708

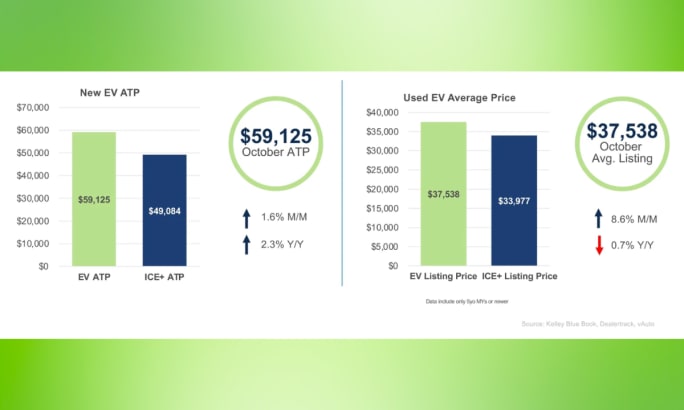

EV Prices Increase Across New and Used Segments

New EV Transaction Prices

The average transaction price (ATP) for new EVs increased to $59,125, up 1.6% month over month and 2.3% year over year. The price premium over ICE+ vehicles widened to $9,359.

Incentives dropped to their lowest level of 2024:

11.1% of ATP

About $6,546 per vehicle

Brands with the highest month-over-month ATP gains:

Porsche: +29.5%

Taycan: +35%

Macan EV: +1.3%

Chevrolet: +5.4%

Cadillac: +5.1%

Tesla’s ATP dipped 1.1% to $53,526, continuing to anchor the lower end of the EV price spectrum.

Average transaction prices for new and used EVs climbed in October, widening the price gap between EVs and ICE models.

Photo: Cox Automotive

Used EV Listing Prices

Used EVs saw a sharp 8.6% month-over-month price jump, reaching an average listing price of $37,538 —still 0.7% below year-ago levels. The increase reopened the price gap with ICE+, which is now $3,561, after near parity in September.

Brands with the largest increases:

Audi: +12.2%

Tesla: +9.5%

Subaru: +9.5%

Chevrolet: +7.8%

Kia: +4.8%

Despite broad increases, 42 models remained under $30,000, with the Nissan Leaf one of the lowest-priced at $12,166.

Days’ Supply Rises for Both New and Used EVs

New EV Days’ Supply

New EV inventory jumped to 79 days in October, up 63.8% from September and down 28% year over year. This follows September’s three-year low of 48 days.

OEMs with the highest supply:

GMC: 91 days

Cadillac: 89 days

Ford: 71 days

Leanest inventory:

Subaru: 8 days

Toyota posted the largest month-over-month increase, rising 33 days to reach 43 days' supply.

Used EV Days’ Supply

Used EV supply increased to 39 days, up from 30 days in September. Inventory remained below ICE+ levels for the eighth time this year.

Supply by brand:

Tightest: Tesla at 29 days

Highest: Genesis at 56 days

GMC and Honda: 55 days each

Volkswagen saw the largest increase, adding 19 days to reach 40 days of supply.

Even with October’s rise, used EV supply remained 19.2% lower than a year ago.

Note: Tesla figures reflect dealer-available inventory, not direct-to-consumer stock.

Market Outlook

October’s sharp reversal signals a recalibration period as EV demand adjusts to post-incentive conditions. The shift is expected to differentiate automakers with strong cost structures from those that depend more on subsidies. Production discipline, competitive pricing, and a focus on consumer confidence will be key as the market settles into a more natural growth trajectory.

More Incentives/Grants

California Governor Approves Instant ZEV Rebates For First-Time Buyers

That instant rebate is the centerpiece of a broader $600 million package Governor Newsom signed into law, keeping California active in the global clean transportation race.

Read More →

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

High Gas Prices Spur EV Sales Rebound

EV sales showed strong month-over-month gains and surging used EV demand, while tighter inventory and declining prices narrowed the gap with gas-powered vehicles.

Read More →

EV Market Resets With Softer Demand, Lower Prices

Near-term EV market performance is expected to remain uneven, while elevated new-vehicle inventory and softer consumer demand may continue to pressure sales and pricing.

Read More →

BBM Launches B2X Rewards, A Gamified Rewards Program For Industry Professionals

Starting Jan. 29, Bobit Business Media's B2B audience readers can earn points for engaging with the content they already trust.

Read More →

2025 Generated Big Headlines In The EV World

The EV industry entered a new more nuanced phase defined by realities and practical outcomes after a few years of grand visions, media hype, and bold investments.

Read More →

California Truck and Bus EV Incentive Program Reopens

GreenPower’s EV Star lineup is eligible for incentives through California’s Clean Truck and Bus Voucher Incentive Project.

Read More →

EV Sales, Days' Supply Show Deepening Downturn

November EV data shows sales falling to multi-year lows as inventory builds and pricing softens following the expiration of federal tax credits.

Read More →

Delaware Offers Extended EV Incentive Programs

Delaware continues to offer rebates for qualifying electric vehicle purchases and Level 2 charger installations through April 30, 2026,

Read More →

How Fleets Can Adjust Approaches To EV Adoption

With the expiration of federal incentives, EV success now hinges less on government policy and more on discounts, battery tech progress, increased range, and broader infrastructure.

Read More →